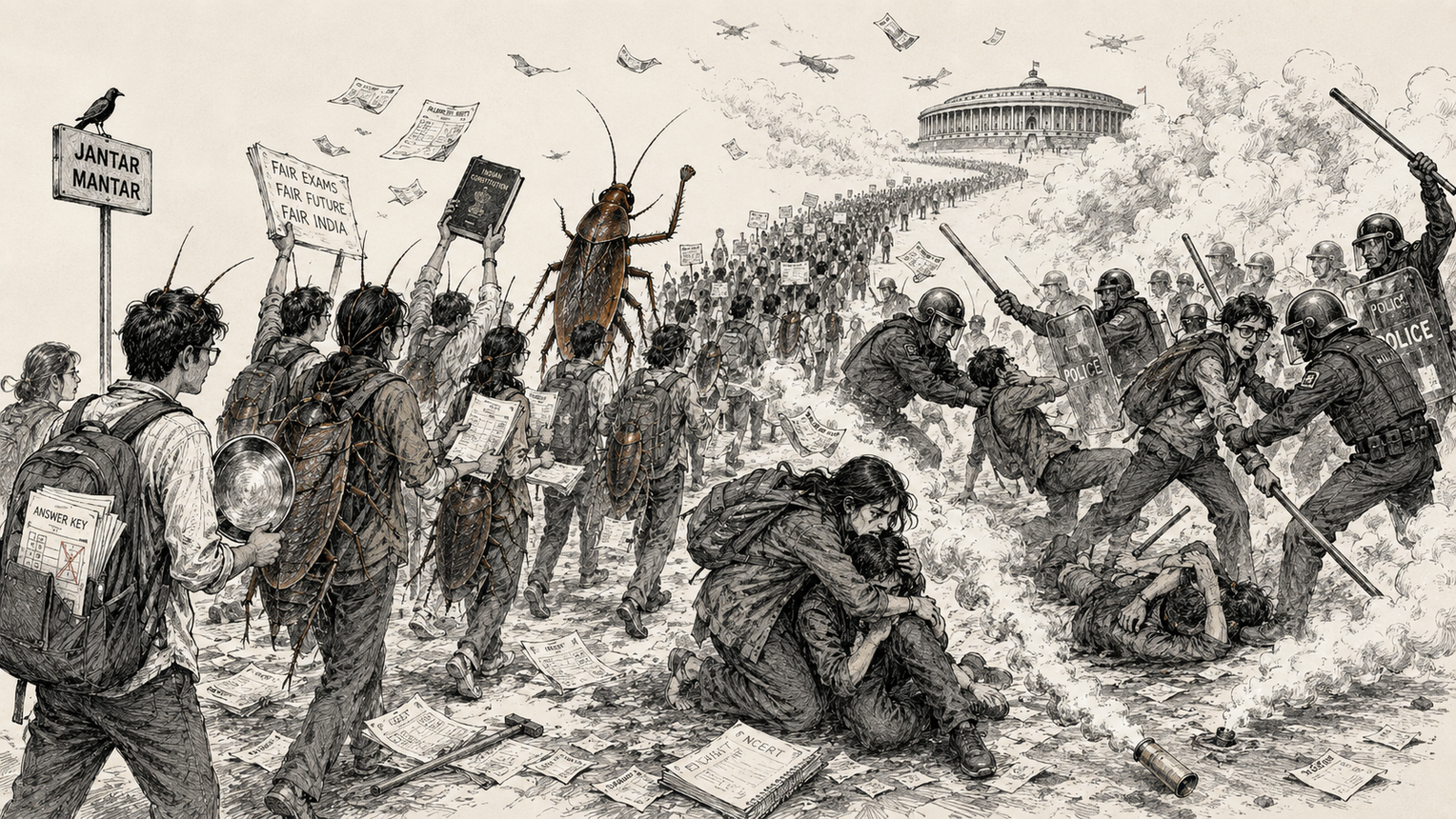

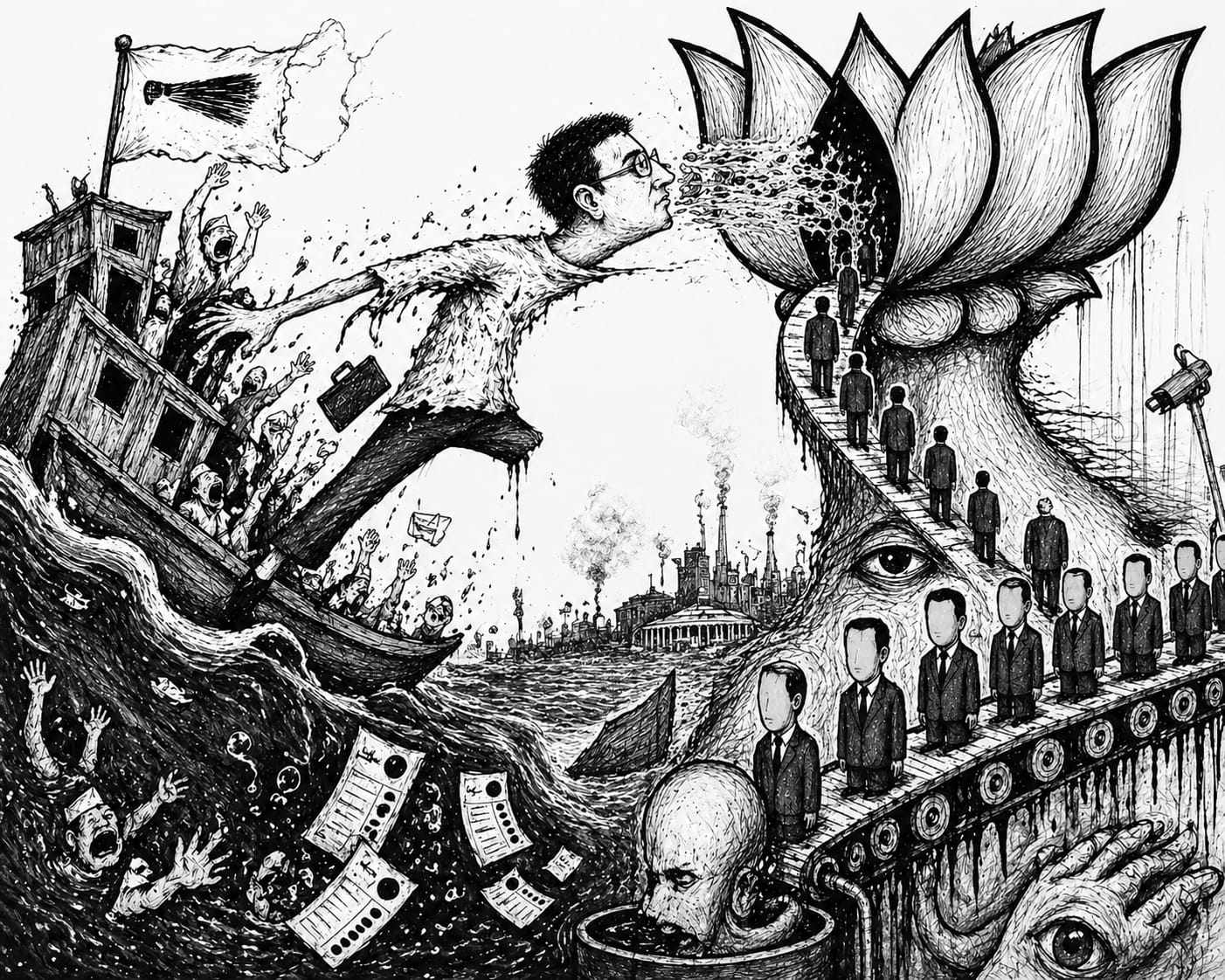

How the Modi government's demonetisation, GST, and COVID lockdown didn't just damage small enterprises—they accelerated the greatest wealth transfer in independent India's history.

The notification arrives at 9:47 P.M.: "Your order is 3 minutes away." Milk, bread, and the tomatoes I forgot to buy. A man on a bike, navigating Delhi's December fog, will materialise at my door before I've put my phone down. I know nothing about him—not his name, not where he's from, not what he did before he started delivering groceries for ₹15 a trip.

But statistically, I can guess. There's a reasonable chance he once worked in a factory that shut down after demonetisation. Or his father ran a kirana store that couldn't survive the arrival of the very app I'm using to summon him. Or he's from one of the 63 lakh informal enterprises that closed between 2015-16 and 2022-23—enterprises that employed 1.6 crore workers who had to go somewhere when the shutters came down.

Quick commerce promises me 10-minute delivery. What it doesn't advertise is what it took to create a labour force willing to bike through smog for piece-rate wages: a decade of systematic destruction of the small enterprise economy that once gave these workers something closer to a livelihood.

This is an essay about that destruction—and about who caused it. It's about how the BJP government spent ten years announcing schemes for MSMEs while delivering ₹1.45 lakh crore annually in corporate tax cuts to their competitors. It's about how three policy shocks—all chosen by the Modi government—didn't just damage small enterprises but accelerated the transfer of market share to favoured conglomerates now building dark stores in every neighbourhood. It's about how the Competition Commission found Amazon and Flipkart guilty of anti-competitive practices—and then this government watched 24 writ petitions stall enforcement.

It is about a number that should concern us: 35,567 MSMEs closed in FY25 alone—47.4% of all closures since the Udyam portal launched in 2020. The crisis isn't stabilising. It's accelerating—and it didn't happen by accident.

The Baseline: What We Had

The NSSO 73rd Round (July 2015-June 2016) provides the definitive pre-shock baseline: 6.34 crore unincorporated enterprises employed 11.13 crore workers across manufacturing (32.4%), trading (34.8%), and services (32.8%). Own Account Enterprises—single-person or family operations without hired workers—constituted 84.2% of all units, employing 62% of workers.

This was India's real employment engine. Not the IT sector that dominates middle-class imagination, not the manufacturing giants that receive policy attention, but the neighbourhood kirana, the two-person welding shop, the tailor operating from a rented room. The sector that never makes it to economic summit panels but employs more Indians than any other.

By 2022-23, the Annual Survey of Unincorporated Sector Enterprises found employment had declined to 10.96 crore—a net loss of 16.45 lakh workers despite population growth. Manufacturing employment specifically fell from 3.6 crore to 3.06 crore, a 15% collapse. India Ratings estimated that without successive shocks, 75 million enterprises would exist today versus the actual 65 million—meaning 10 million enterprises were lost.

The informal sector's Gross Value Added growth collapsed from +7.4% CAGR (2010-16) to -0.2% post-2016. That's not a slowdown. That's a recession hidden inside headline GDP growth.

Three Shocks, One Architect

The destruction of India's MSME sector wasn't an accident of history or an unfortunate confluence of global forces. It was the direct consequence of three policy decisions, all made by the same government, all implemented with the same combination of hubris and incompetence.

Demonetisation: Modi's "Surgical Strike" on the Poor

On 8 November 2016, Prime Minister Narendra Modi appeared on television to announce that 86% of India's currency would be invalidated at midnight, with four hours' notice. He called it a "surgical strike on black money." He asked the nation to endure 50 days of hardship for the greater good. He promised that black money hoarders would be exposed, terrorism would be defunded, and a new digital economy would emerge.

None of it happened. The RBI later confirmed that 99.3% of demonetised currency returned to the banking system—meaning the "black money" was either never there or successfully laundered. But the damage to small enterprises was immediate and catastrophic. The All India Manufacturers Organisation reported 60% job losses in small-scale traders, shops, and micro industries during the first 50 days—compared to just 2% in large-scale industries. In Ludhiana, over 70% of the city's 12,000 hosiery factories shut down, throwing 400,000 people out of work.

Former Prime Minister Manmohan Singh, the economist who designed India's 1991 liberalisation, took to Parliament to deliver a verdict that history has vindicated: "This is a monumental management failure and, in fact, it is a case of organised loot and legalised plunder."

The asymmetry was structural and predictable. Large corporations had access to banking infrastructure, credit lines, and digital payment systems. The kirana store owner paying daily wages in cash, the construction contractor settling with labourers at day's end, the vegetable vendor operating entirely outside the formal financial system—they had nothing. Modi's decision didn't hurt them by accident. It hurt them because the government either didn't think about them or didn't care.

GST: Death by Compliance

If demonetisation was a sudden blow, GST was a slow strangulation. The Goods and Services Tax, implemented in July 2017 while businesses were still recovering from the currency crisis, imposed compliance burdens that large corporates could absorb and small enterprises could not.

The BJP government rushed the implementation, ignored warnings about complexity, and created a system that required multiple filings, digital infrastructure that didn't exist in much of India, and professional assistance that small businesses couldn't afford. The "one nation, one tax" slogan masked a nightmare of multiple rate slabs, frequent rule changes, and a compliance architecture designed for corporate India.

The economics was brutally simple. The survival of the next-door kirana shop often depended on operating at the margins of formal compliance; only by doing so could they offer competitive prices against larger players with economies of scale. GST eliminated that margin while imposing paperwork requirements that either required hiring accountants or required spending hours on compliance instead of running the business.

The CAG's 2019 compliance audit documented widespread implementation failures. But the deeper problem was political choice: a tax system built for Ambani and Adani imposed on an economy that was 90% informal.

COVID Lockdown: Four Hours' Notice, Again

On 24 March 2020, Prime Minister Modi appeared on television again. At 8 P.M., he announced that the country would enter a complete lockdown at midnight—four hours' notice, the same as during demonetisation. The world's largest democracy was shutting down with less warning than a restaurant gives for a reservation cancellation.

The images that followed—millions of migrant workers walking hundreds of kilometres on highways, carrying children and possessions, dying on the roads—were not aberrations. They were the logical consequence of a government that had spent four years weakening small enterprises' capacity to survive shocks, followed by a decision that gave them no time to prepare.

The lockdown was announced without consulting state governments, without arranging transport for stranded workers, without planning for food distribution, and without considering the tens of millions who lived hand-to-mouth in the informal economy. The virus was real; the policy response was a choice. Other countries locked down with support systems in place. India imposed a lockdown and instructed workers to walk.

According to India Ratings, the cumulative impact of these three shocks amounts to Rs 11.3 lakh crore in economic losses—equivalent to 4.3% of FY23 GDP. Three decisions. One government. Sixty-three lakh enterprises destroyed.

Make in India, Break in India

Before examining the credit squeeze that starved small enterprises of capital, it's worth pausing on the slogan that was supposed to save them.

On 25 September 2014, four months after taking office, Prime Minister Modi launched "Make in India" with characteristic bombast—the promise: 100 million manufacturing jobs by 2022. Manufacturing would rise from 16% to 25% of GDP. India would become "the new factory of the world."

A decade later, the reality: manufacturing's share of GDP has fallen to 14%—lower than when Modi took office. Manufacturing jobs have collapsed from 5.1 crore in 2016-17 to 2.7 crore in 2020-21. Instead of 100 million new jobs, we have lost 24 million existing ones. The Make in India logo, ironically, was designed by an American firm for Rs 11 crore. That tells you everything about the gap between branding and substance.

But here's what matters for this essay: while Make in India failed to create manufacturing jobs, it succeeded spectacularly at something else—concentrating manufacturing in the hands of large players who could navigate the compliance maze and access the credit that small enterprises couldn't.

The Credit Squeeze: Who Gets Money, Who Doesn't

While small enterprises were dying, the government's response was a parade of schemes that looked impressive on paper and delivered almost nothing on the ground.

The SIDBI-Crisil May 2025 report provides the most comprehensive credit gap analysis to date. Overall MSME finance demand stands at ₹123 lakh crore, with addressable debt demand at ₹64 lakh crore. Formal debt supply reaches only ₹34 lakh crore—leaving a ₹30 lakh crore credit gap. Only 19% of MSME credit demand is met by formal sources.

Of 6.35 crore Udyam-registered MSMEs, only 3.68 crore have ever accessed formal credit. Ever. In their entire existence.

The flagship Emergency Credit Line Guarantee Scheme (ECLGS), announced with much fanfare during the COVID-19 pandemic, promised ₹5 lakh crore in credit guarantees. Actual disbursement: ₹2.93 lakh crore—41% unutilised. The Subordinate Debt Scheme targeted 2 lakh stressed MSMEs with a total of ₹20,000 crore. Actual delivery: 756 MSMEs received ₹81.78 crore. That's a 99.6% shortfall.

Now compare this to what happened for large corporations.

In September 2019, Finance Minister Nirmala Sitharaman announced corporate tax cuts that would cost the exchequer ₹1.45 lakh crore annually. She said it would "boost employment and economic activity." The Sensex surged 1,900 points in a single day—the largest single-day gain in a decade. Markets understood who was being served.

The Parliamentary panel later documented that the exchequer lost Rs 1.84 lakh crore in just two years. The top 0.9% of companies benefited most. The 99.1% of companies with turnover below Rs 400 crore were already taxed at lower rates. The windfall went to those who needed it least—and who had the most access to the Prime Minister's Office.

This is the arithmetic of the Modi government's economic policy: ₹1.45 lakh crore annually to large corporates versus a 99.6% shortfall on the ₹20,000 crore promised to stressed MSMEs. The choice is explicit. The beneficiaries are clear.

The Concentration Machine: Who Benefits from MSME Destruction

The small enterprise crisis isn't happening in isolation. It's happening alongside—and directly because of—an unprecedented concentration of corporate power in the hands of a few conglomerates with well-documented proximity to the ruling party.

The 20 most profitable firms in India now generate approximately 70% of the country's profits, up from 14% three decades ago. The Herfindahl-Hirschman Index (HHI) across eight major sectors reached 2,532 in FY25—crossing the "highly concentrated" threshold of 2,500 for the first time in over a decade.

Consider the sectors where concentration has accelerated under the BJP rule:

Telecom: Three-player oligopoly. Reliance Jio's entry, backed by regulatory advantages and capital that dwarfed competitors, wiped out a dozen players and now dominates a market that once had fifteen operators.

Aviation: Effective duopoly. IndiGo and the Tata-owned Air India (which acquired AirAsia India and Vistara) control over 90% of domestic traffic. Parliament has issued warnings about concentration.

Ports: Adani Ports commands 27.8% of Indian cargo and 45.2% of container traffic.

Airports: Adani controls seven operational airports, which handle 25% of passenger traffic and 33% of air cargo, making it India's largest and the world's third-largest airport operator. These airports were acquired through privatisation processes that opposition parties have repeatedly questioned.

E-commerce: Amazon and Flipkart control 70-80% of the market—and have now been found by the CCI to have systematically disadvantaged small sellers.

The pattern is consistent: sectors that once had distributed ownership are consolidating into oligopolies controlled by a handful of business houses. The names that keep appearing—Reliance, Adani, Tata—are not random. They represent a political economy in which access to the PMO correlates closely with access to capital, contracts, and regulatory forbearance.

Jairam Ramesh, responding to the 2019 corporate tax cut, called it a decision by a "headline-itis afflicted, panic-stricken Modi Sarkar" that would benefit a few large conglomerates while doing nothing to revive investment. He was right. Private investment didn't revive. Stock markets boomed. The gap between corporate India and small enterprise India widened further.

The CCI Investigation: Justice Delayed by Design

In January 2020, the Competition Commission of India ordered an investigation into Amazon and Flipkart based on a complaint from the Delhi Vyapar Mahasangh, a traders' association representing the 80 million retailers that CAIT claims as members. The allegation is that the platforms were giving preferential treatment to select sellers, thereby creating a two-tier marketplace in which ordinary sellers remained "mere database entries."

In August 2024, the CCI's investigation concluded. The findings were damning. According to reports reviewed by Reuters, Amazon operated with 6 preferred sellers and Flipkart with 33 preferred sellers who received marketing, warehousing, and other services at "minuscule cost." Both platforms were found to have violated competition laws through deep discounting, exclusive launches, and preferential treatment that "forecloses competition."

The CCI produced a 1,027-page report on Amazon and a 1,696-page report on Flipkart. The evidence was comprehensive. The violations were clear.

And then? Twenty-four writ petitions were filed across Karnataka, Telangana, Madras, Delhi, Allahabad, and the Punjab and Haryana High Courts by Amazon, Flipkart, Samsung, Vivo, and their associated sellers. The case has been bouncing between courts for four years. The CCI has had to go to the Supreme Court just to get the cases consolidated.

Four years of investigation. Comprehensive findings of violation. Zero enforcement. Zero penalties. Zero consequences.

This is what happens when a government talks about "ease of doing business" while making it impossible for regulators to do their jobs. Union Commerce Minister Piyush Goyal publicly stated that Amazon engages in predatory pricing that harms small sellers. His own government's competition regulator found exactly that. And yet nothing happens—because the same government that claims to champion small traders has created a legal architecture where findings never become consequences.

The traders who filed the original complaint in 2020 are still awaiting a decision. Many of their shops have closed in the interim. The platforms they accused continue to operate exactly as before.

Quick Commerce: The Next Wave of Destruction

While the CCI case stalls, the next wave of MSME destruction is already underway—led by familiar names with familiar political connections.

The All India Consumer Products Distributors Federation reported that the rapid growth of quick commerce led to approximately 200,000 kirana stores closing in one year. Metro cities saw 90,000 closures, Tier-I cities 60,000, Tier-II and Tier-III towns 50,000.

RedSeer Consulting projects that quick commerce may put 25% of India's kirana stores out of business by 2030.

The mechanisms are familiar: deep discounting that burns investor capital to undercut prices, delivery speeds that require dark-store infrastructure that small retailers can't match, exclusive brand partnerships that lock kiranas out of popular products.

"In five years, it'll all be over," PP Patel, owner of Rex General Store in Mumbai, told Rest of World. He's not being pessimistic. He's reading the market.

And who is leading this charge? Reliance JioMart now operates more than 600 dark stores across 1,000+ cities. Q1 FY26 recorded 5.8 million new users and 200% year-on-year growth in daily orders. The company whose chairman is photographed with the Prime Minister more frequently than most cabinet ministers is now competing directly with the neighbourhood kirana for your tomatoes.

Blinkit (owned by Zomato), Zepto, and Swiggy Instamart complete the oligopoly. Together, they're burning billions to create a market structure where small retailers cannot survive. The government that claims to stand for small traders watches silently—occasionally making noises about regulation that never materialise into action.

This isn't the invisible hand of the market. This is capital-backed incumbents using regulatory indulgence to destroy distributed retail. When the destruction is complete, the oligopoly will raise prices. By then, there will be no kiranas left to compete.

The Accelerating Crisis

The Udyam portal data tells the story of acceleration under BJP rule:

FY 2020-21: 175 closures

FY 2021-22: 6,222 closures

FY 2022-23: 13,290 closures

FY 2023-24: 19,828 closures

FY 2024-25 (to February): 35,567 closures

Total closures since July 2020: 75,082 enterprises. Jobs lost from 49,342 closures tracked through July 2024: 3.18 lakh.

FY25 alone accounts for 47.4% of all closures since the portal launched. The crisis isn't stabilising. It's compounding—eleven years into BJP rule, with no course correction in sight.

The government attributes closures to "ownership changes and duplicate registrations"—a bureaucratic deflection from a government that has made an art of changing definitions to obscure failures. Industry experts cite rising operational costs, raw material shortages, lack of skilled labour, and complex regulatory policies. Neither explanation accounts for the doubling of the rate year over year.

The Compliance Trap Continues

The pattern of imposing formal-sector compliance burdens on informal-sector enterprises—the same pattern that made demonetisation and GST catastrophic—continues to claim victims.

Only 25-26% of 6,500 MSME pharma units are expected to meet GMP Schedule M compliance norms by the 31 December 2025 deadline. Approximately 4,300 MSMEs have failed to take the required steps and risk closure. Gujarat shows 98.8% compliance; other states lag significantly—another example of how compliance-heavy policy works for states with strong industrial infrastructure and destroys enterprises everywhere else.

Meanwhile, 6,385 recognised startups have closed by October 2025. Karnataka leads with 845 closures (4.1% of its 20,745 startups), followed by Maharashtra with 1,200 closures and Delhi with 737. So much for "Startup India."

The Budget 2025-26 announced threshold changes that will allow more enterprises to qualify as MSMEs—investment ceilings increased by 2.5× and turnover ceilings doubled. This is classic BJP economic policy: change the definition of success rather than achieve it. Whether this reclassification exercise translates into actual support remains to be seen. The track record—Make in India, Skill India, Startup India, MUDRA—suggests it won't.

What Would It Take?

The solutions are not mysterious. They require political will, which this government has shown no interest in developing, because the current architecture serves the interests for which it was designed.

First, enforce existing laws. The CCI investigation found clear violations. Enforce the findings. The Inter-State Migrant Workmen Act mandates protections for workers. Enforce it. The problem isn't the absence of law—it's a government that enforces laws selectively based on who's being regulated.

Second, redirect fiscal priorities. The ₹1.45 lakh crore annual corporate tax cut could fund the entire credit gap for MSMEs if redirected. It won't be—because this government has made clear who it serves. But the choice should be visible. Every budget that renews corporate tax benefits while announcing yet another credit scheme with 99% shortfall is making a distributional decision. Voters should understand the decision.

Third, address concentration directly. Break up oligopolies. Mandate interoperability in e-commerce. Prevent infrastructure capture by single conglomerates. The tools exist in competition law; they require a government willing to use them against its allies.

Fourth, count properly. The 2026 National Migration Survey is a start. But we need continuous tracking of enterprise formation and closure, employment generation and loss, credit access and denial. You cannot address what you refuse to measure—and this government has shown a remarkable talent for not measuring what it doesn't want to see.

Fifth, recognise the politics. Small enterprises don't have lobbyists. Their owners don't attend Vibrant Gujarat summits or fund electoral bonds. Their workers don't vote where they work. The political economy is stacked against them. Changing it requires building constituencies that currently don't exist—and voting out a government that has spent a decade serving the opposite interests.

The Transfer

Here's the pattern of the Modi decade: three shocks weaken small enterprises. The policy response favours large corporations through tax cuts and access to credit, while regulatory enforcement against platform giants lags. Market concentration accelerates—the share of small enterprises in employment and output declines. Large corporate share of profits grows. Favoured business houses expand into sector after sector.

The 20 most profitable firms, which capture 70% of profits, compared with 14% three decades ago, isn't a market outcome. It's a policy outcome. It's what happens when you design a tax system for corporations, a compliance system for corporations, and a credit system for corporations, and then impose them on an economy where 99% of enterprises are micro. It's what happens when you govern for Dalal Street while giving speeches about chai wallahs.

I order my groceries on an app. They arrive in 10 minutes. The man who delivers them might once have owned a shop, or worked in a factory, or had a job with a future. Now he's a gig worker in a company valued in the billions, delivering tomatoes for ₹15 a trip, hoping the algorithm sends him enough orders to make rent.

This is the Great Indian MSME destruction—and the Modi government built it. Sixty-three lakh enterprises closed. 1.6 crore jobs lost. A credit gap of ₹30 lakh crore persists, with 35,567 closures in FY25 alone. The top 20 companies capturing 70% of profits. CCI findings gathering dust behind 24 writ petitions. Make in India became Break in India. Additionally, 200,000 more kirana stores closed this year, with 25% of those remaining projected to close by 2030.

The trajectory is clear. The responsibility is clear. Without fundamental political change, India's distributed economic structure faces an existential threat.

The delivery notification pings again. My order has arrived. The man is already gone, biking to his next ₹15.

Data sources: India Ratings and Research (July 2024); SIDBI-Crisil Credit Gap Analysis (May 2025); Ministry of MSME Udyam Portal data; NSSO 73rd Round (2015-16); Annual Survey of Unincorporated Sector Enterprises (2022-23); CCI Case No. 40 of 2019; AICPDF reports; Business Standard HHI analysis; Parliamentary Standing Committee reports; RBI KLEMS database.

Write a comment ...